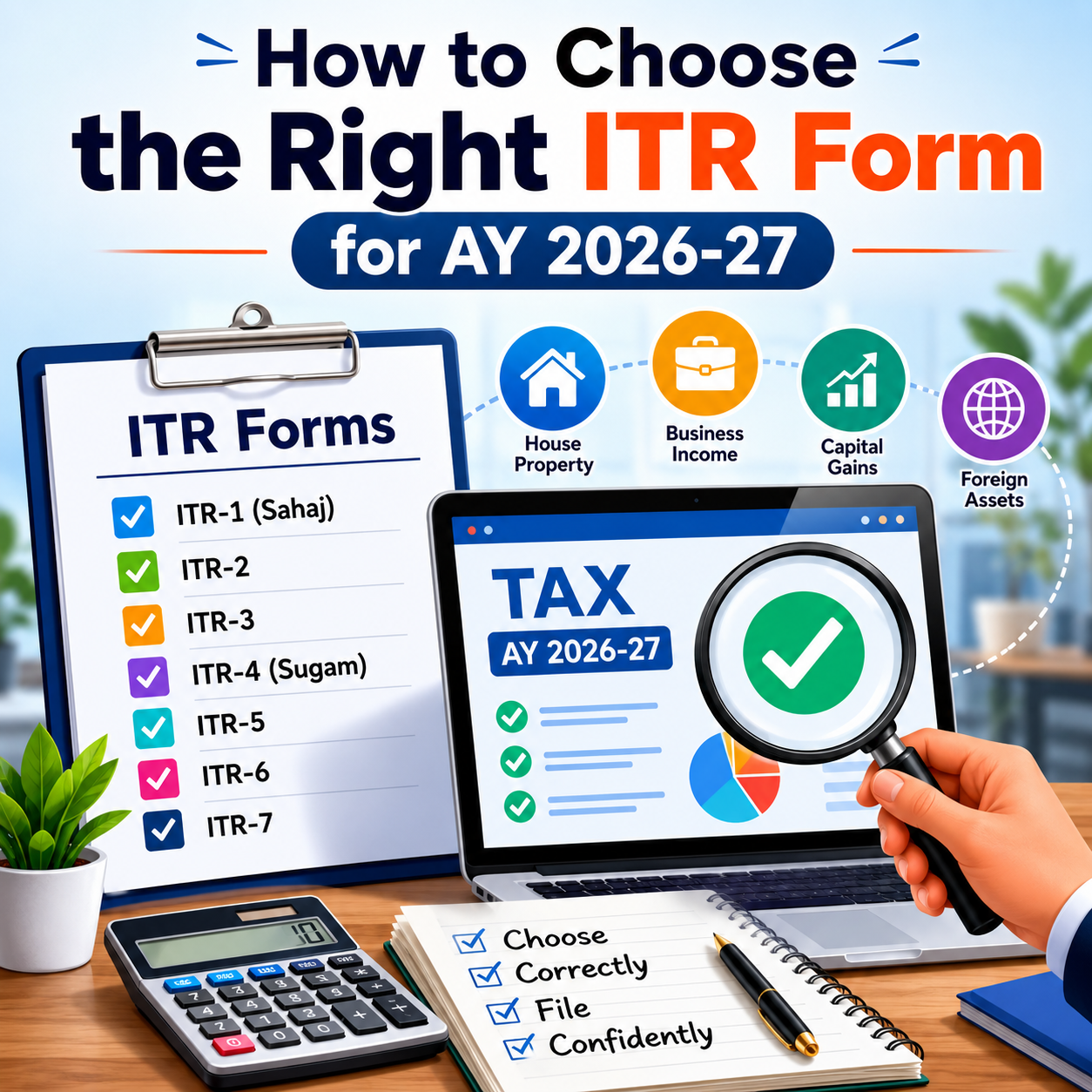

Complete Guide to Selecting the Proper ITR Form for AY 2026-27

How to Select the Right ITR Form for AY 2026-27

The filing season for Income Tax Returns (ITR) for Assessment Year (AY) 2026-27 is now open. One of the most frequent errors made by taxpayers is choosing an inappropriate ITR form while filing their return. Using the wrong form may cause the return to be considered defective, resulting in notices from the Income Tax Department and additional compliance requirements.

To ensure smooth and accurate filing, taxpayers should understand the eligibility criteria for each ITR form. This article highlights the key changes introduced for AY 2026-27 and explains who can use ITR-1 (Sahaj).

Major Updates for AY 2026-27

Before filing your return, it is important to be aware of the following changes applicable for the current assessment year.

1. Reporting of Two House Properties Allowed in ITR-1 and ITR-4

The government has provided relief to small taxpayers by allowing eligible individuals filing ITR-1 (Sahaj) and ITR-4 (Sugam) to disclose income from up to two house properties, provided all other prescribed conditions are fulfilled.

2. Updated Return Filing Deadlines

The due dates for filing Income Tax Returns for AY 2026-27 are as follows:

| Taxpayer CategoryDue Date | |

| Individuals/HUFs not subject to audit and not having business or professional income | 31 July 2026 |

| Taxpayers having business or professional income but not liable for audit | 31 August 2026 |

| Taxpayers covered under tax audit provisions | 31 October 2026 |

Filing within the prescribed timeline helps avoid interest, penalties, late filing fees, and other inconveniences.

ITR-1 (SAHAJ)

Eligibility for Filing ITR-1

A resident individual may file ITR-1 if he or she has:

- Income from salary or pension.

- Income from not more than two house properties.

- Income from other sources such as savings bank interest, fixed deposit interest, family pension, etc.

- Agricultural income not exceeding ₹5,000.

- Total income up to ₹50 lakh.

- Long-term capital gains under Section 112A up to ₹1,25,000.

Persons Not Eligible to File ITR-1

ITR-1 cannot be used by a taxpayer who:

- Has total income exceeding ₹50 lakh.

- Is a director in any company.

- Owns unlisted equity shares.

- Has capital gains income not covered under the prescribed conditions.

- Earns income from business or profession.

- Possesses foreign assets or receives foreign income.

- Is a Non-Resident (NR) or Resident but Not Ordinarily Resident (RNOR).

Best Suited For

ITR-1 is generally suitable for:

- Salaried individuals.

- Retired pensioners.

ITR-2

Who is Eligible to File ITR-2?

ITR-2 is meant for Individuals and Hindu Undivided Families (HUFs) who do not have income from business or profession but earn income from one or more of the following sources:

- Salary or pension.

- Income from house property.

- Capital gains arising from the sale of shares, mutual funds, immovable property, or other capital assets.

- Foreign income or ownership of foreign assets.

- Total income exceeding ₹50 lakh.

- Holding the position of Director in a company.

- Investment in unlisted equity shares.

Who Should Use ITR-2?

ITR-2 is generally suitable for:

- Salaried individuals having capital gains transactions.

- Taxpayers who have sold property, shares, mutual funds, or other capital assets during the financial year.

- Non-Resident Indians (NRIs).

- Individuals required to disclose foreign assets or foreign-source income in their Income Tax Return.

- Taxpayers earning interest from bank deposits and other similar sources.

ITR-3

Who Can File ITR-3?

ITR-3 is applicable to Individuals and Hindu Undivided Families (HUFs) who earn income from business or professional activities. This includes income from:

- Proprietary business operations.

- Professional services and practice.

- Freelancing assignments.

- Commission or brokerage earnings.

- Futures and Options (F&O) trading.

- Intraday stock trading.

- Business or professional income along with income from salary, house property, capital gains, or other sources.

Who Should Use ITR-3?

ITR-3 is generally suitable for:

- Chartered Accountants.

- Doctors and medical practitioners.

- Advocates and legal professionals.

- Consultants and independent professionals.

- Share and derivatives traders.

- Freelancers.

- Proprietors running their own business.

ITR-4 (SUGAM)

Who Can File ITR-4?

ITR-4 is designed for Resident Individuals, HUFs, and Firms (excluding LLPs) who opt for the presumptive taxation scheme under:

- Section 44AD – Presumptive taxation for eligible businesses.

- Section 44ADA – Presumptive taxation for specified professionals.

- Section 44AE – Presumptive taxation for goods carriage operators.

Eligibility Conditions for ITR-4

A taxpayer can file ITR-4 if:

- Total income does not exceed ₹50 lakh.

- Income is declared under the eligible presumptive taxation provisions.

- Income is earned from up to two house properties.

- Income includes interest and other permissible sources.

- Long-Term Capital Gain (LTCG) under Section 112A does not exceed ₹1,25,000.

Who Cannot File ITR-4?

ITR-4 cannot be used by:

- Taxpayers holding foreign assets or earning foreign income.

- Directors in companies.

- Limited Liability Partnerships (LLPs).

Who Should Use ITR-4?

ITR-4 is best suited for:

- Small business owners opting for presumptive taxation.

- Tax practitioners and consultants.

- Professionals covered under Section 44ADA.

- Retail traders and other eligible taxpayers under the presumptive taxation scheme.

ITR-5

Who Can File ITR-5?

ITR-5 is applicable to various non-individual entities, including:

- Partnership Firms.

- Limited Liability Partnerships (LLPs).

- Associations of Persons (AOPs).

- Bodies of Individuals (BOIs).

- Artificial Juridical Persons (AJPs).

This return form is not meant for individual taxpayers.

ITR-6

Who Can File ITR-6?

ITR-6 is required to be filed by companies that are not claiming exemption under Section 11 of the Income Tax Act.

This form is commonly used by:

- Private Limited Companies.

- Public Limited Companies.

- Other corporate entities not eligible for filing ITR-7.

ITR-7

Who Can File ITR-7?

ITR-7 is prescribed for entities that are required to furnish returns under specific provisions of the Income Tax Act. These generally include:

- Charitable Trusts.

- Religious Trusts.

- Political Parties.

- Educational and Academic Institutions.

- Research Associations and similar organizations.

Consequences of Choosing the Wrong ITR Form

Filing an incorrect ITR form can create unnecessary complications and may result in various issues such as:

- Receipt of a defective return notice under Section 139(9).

- Delay in processing of the Income Tax Return.

- Delay in receiving income tax refunds.

- Additional compliance and rectification requirements.

- Necessity to file a revised return.

Therefore, taxpayers should carefully assess all sources of income and verify their eligibility before selecting the applicable return form.

Conclusion

Selecting the correct ITR form is one of the most crucial steps in the return filing process. For AY 2026-27, taxpayers should take note of important updates, including the relaxation allowing eligible taxpayers to report income from up to two house properties and the revised return filing deadlines for different categories of taxpayers.

Before filing the return, it is advisable to review all sources of income, including salary, house property, capital gains, business income, professional receipts, foreign assets, foreign income, and presumptive taxation income. Choosing the appropriate ITR form ensures accurate compliance with tax provisions and reduces the chances of notices, delays, and filing errors.

A correctly filed Income Tax Return not only fulfills legal obligations but also facilitates quicker processing of returns and faster issuance of refunds.