Income Tax Department Enables ITR-3 for AY 2026-27; ITR-1 to ITR-4 Ready for Filing

ITR-3 Now Available for AY 2026-27: Online Filing & Excel Utility Released

The Income Tax Department has officially activated both the Online Filing Facility and Excel Utility for ITR-3 for Assessment Year (AY) 2026-27. This marks a significant milestone for taxpayers who were waiting for the ITR-3 form to become available before submitting their Income Tax Returns.

Previously, the department had already enabled ITR-1, ITR-2, and ITR-4 in both online and offline modes. However, many taxpayers—including business owners, professionals, freelancers, traders, and individuals earning business or professional income—were unable to file their returns because ITR-3 had not yet been released.

With ITR-3 now available, the majority of individual taxpayers can begin filing their Income Tax Returns for AY 2026-27 without any further delay.

Taxpayers can access the filing portal by visiting www.incometax.gov.in.

Extended Due Date for Certain ITR-3 Filers

Individuals filing ITR-3 who earn income from business or profession and are not required to get their accounts audited can file their Income Tax Return up to 31st August 2026.

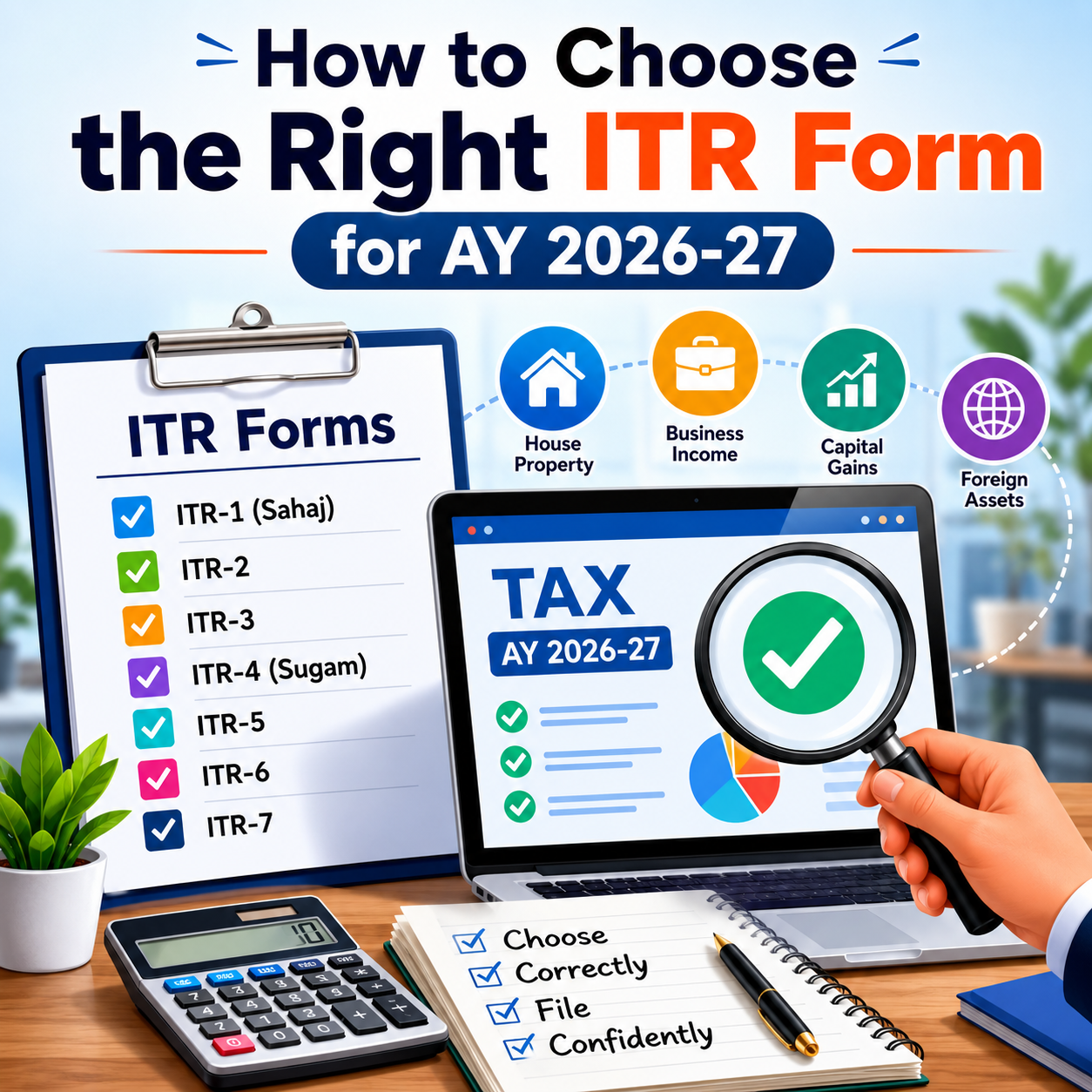

Who Should File ITR-3?

ITR-3 is applicable to Individuals and Hindu Undivided Families (HUFs) having income from business or profession, including:

- Proprietorship business

- Professional practice

- Freelancing services

- Share trading and Futures & Options (F&O) transactions

- Commission or brokerage income

- Business income along with income from other sources

In general, taxpayers earning income under the head “Profits and Gains of Business or Profession” should file ITR-3, unless they choose the presumptive taxation scheme and qualify to file ITR-4.

Who Should File ITR-1?

ITR-1 (Sahaj) is meant for resident individuals who satisfy the prescribed conditions and generally have:

- Income from salary or pension

- Income from one house property

- Income from other sources, such as interest

- Total income within the prescribed eligibility limits

Who Should File ITR-2?

ITR-2 is meant for Individuals and Hindu Undivided Families (HUFs) who do not earn income from business or profession but have income from one or more of the following sources:

- Capital gains arising from the sale of shares, mutual funds, or immovable property.

- Income from more than one house property.

- Ownership of foreign assets or receipt of foreign income.

- Total income that exceeds the eligibility criteria prescribed for filing ITR-1.

Who Should File ITR-3?

ITR-3 is designed for Individuals and Hindu Undivided Families (HUFs) earning income from a business or profession. It is generally applicable to taxpayers such as:

- Proprietors running a business.

- Professionals, including doctors, lawyers, architects, and chartered accountants.

- Consultants providing professional services.

- Freelancers earning income from independent assignments.

- Traders dealing in shares, Futures & Options (F&O), and other derivatives.

- Individuals having business or professional income along with salary, capital gains, house property income, or income from other sources.

Documents Required Before Filing Your Income Tax Return

To ensure a smooth and accurate filing process, taxpayers should keep the following documents readily available:

- PAN Card

- Aadhaar Card

- Form 16 (where applicable)

- Form 26AS

- Annual Information Statement (AIS)

- Taxpayer Information Summary (TIS)

- Bank account details

- Capital gains statements

- Interest certificates from banks and financial institutions

- Business financial statements and books of accounts (where applicable)

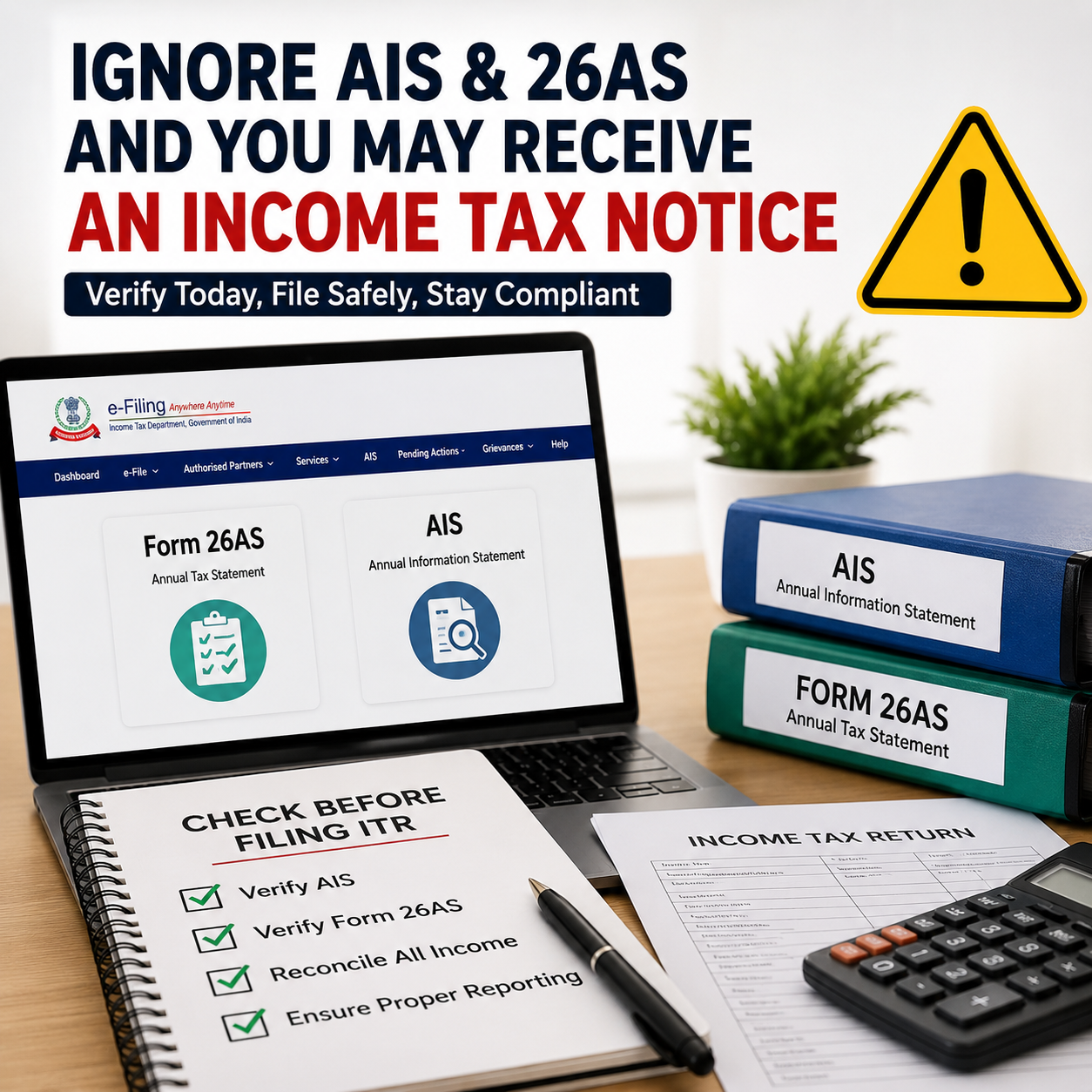

Verify AIS, TIS and Form 26AS Before Filing

Before submitting the Income Tax Return, taxpayers should carefully reconcile the information available in:

- Annual Information Statement (AIS)

- Taxpayer Information Summary (TIS)

- Form 26AS

These records provide details of various financial transactions, including:

- Interest income

- Dividend income

- Share market transactions

- Mutual fund investments and redemptions

- Sale or purchase of property

- Tax Deducted at Source (TDS)

- Specified high-value financial transactions

Matching these details with the information reported in your return helps avoid discrepancies. Any inconsistency may lead to notices from the Income Tax Department, defective return processing, or additional compliance requirements.

E-Verification is Compulsory

Filing the Income Tax Return is only one part of the process. Taxpayers must also complete the e-verification of the return within the prescribed time limit.

A return that is not e-verified within the specified period may be treated as invalid under the provisions of the Income-tax Act, resulting in the return being considered as not filed.

ITR-3 Now Available Along with ITR-1, ITR-2 & ITR-4

The launch of ITR-3 for AY 2026-27 has provided significant relief to business owners, professionals, freelancers, traders, and other taxpayers who were waiting for the form to become available before filing their Income Tax Returns.

With ITR-1, ITR-2, ITR-3, and ITR-4 now enabled in both online and offline modes, the majority of taxpayers can move forward with filing their returns for the current assessment year.

Before Filing

-

Review AIS (Annual Information Statement)

-

Verify TIS (Taxpayer Information Summary)

-

Reconcile details with Form 26AS