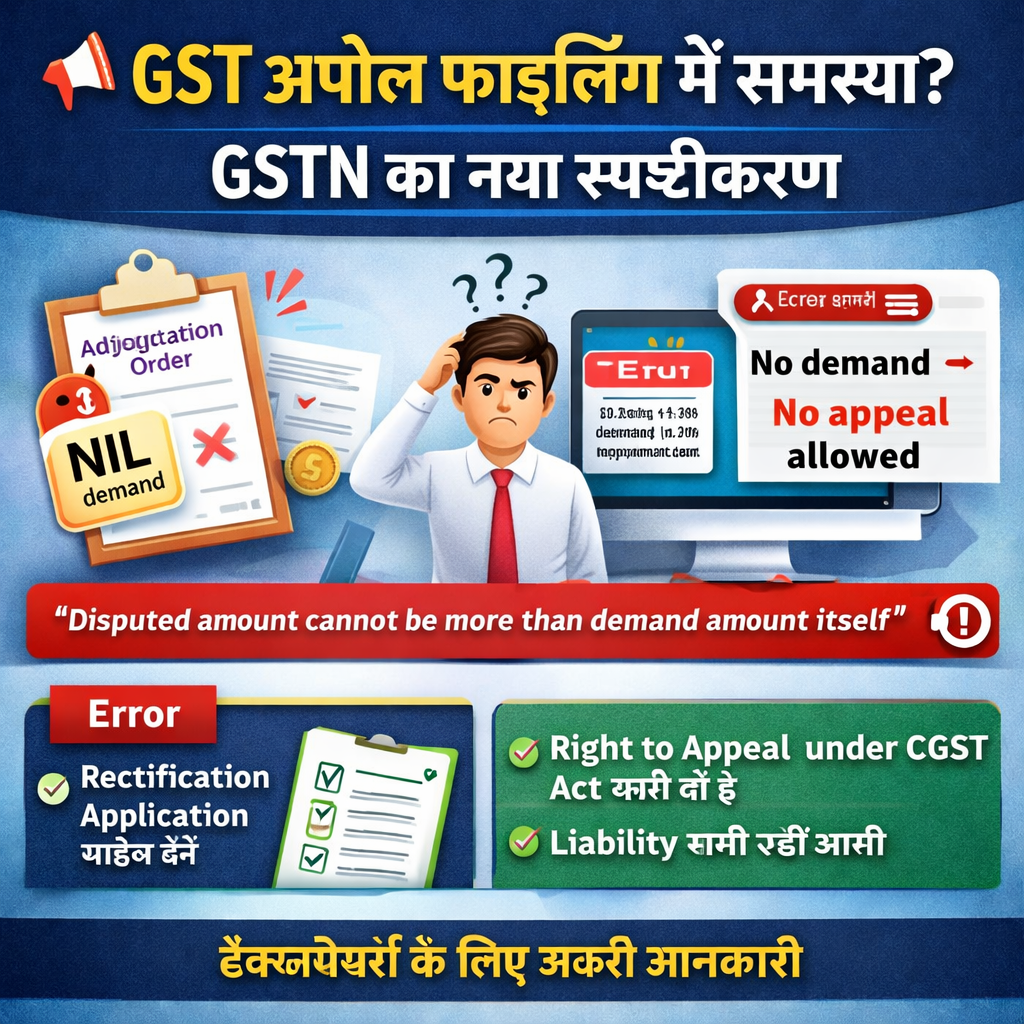

GST Update: Filing Error in GST Appeals Successfully Resolved

GST Update: Relief in Pre-Deposit Requirement While Filing Appeals

A key and practical update has been introduced on the GST portal concerning the pre-deposit requirement for filing appeals. This change directly benefits taxpayers filing appeals in Form APL-01 and resolves several long-standing practical issues.

🔍 Background – Pre-deposit under GST

As per CGST Act, 2017, Section 107(6), any taxpayer filing an appeal before the Appellate Authority must make a mandatory pre-deposit comprising:

✅ Full payment of admitted tax liability

✅ 10% of the disputed tax amount (subject to prescribed limits)

This payment is a prerequisite for the admission of an appeal.

⚠️ Earlier Issue on GST Portal

Previously, while filing Form APL-01, the GST portal:

- Automatically calculated the 10% pre-deposit

- ❌ Did not allow editing of this field

This led to several practical difficulties for taxpayers.

❗ Common Challenges Faced

- Pre-deposit already paid through DRC-03 or other modes

- Incorrect classification of demand under wrong tax heads

- Partial payments not considered by the system

- Cases involving only interest or penalty disputes

- Differences in interpretation of disputed tax amount

👉 As a result, taxpayers often faced duplication of payments or incorrect calculations.

✅ Latest Update (Effective 6 April 2026)

The GSTN has now provided significant relief:

🔹 Key Change

👉 The pre-deposit percentage field is now editable in Form APL-01

🎯 Impact on Taxpayers

With this update, taxpayers can now:

✔️ Adjust pre-deposit based on actual liability

✔️ Consider payments already made

✔️ Avoid excess or duplicate payments

✔️ Accurately compute disputed tax amounts

✔️ File appeals aligned with actual case facts

🧾 Practical Situations Where This Helps

1. Pre-deposit Already Paid

Taxpayers can reduce the payable amount in APL-01 if already paid via DRC-03

2. Incorrect Demand Reflection

System-generated demand can now be corrected

3. Appeals for Interest/Penalty Only

No need to apply 10% on the entire demand

4. Partial Appeals / Multiple Orders

Pre-deposit can be calculated proportionately

⚖️ Important Safeguard

👉 This flexibility is subject to verification by the Appellate Authority, including:

- Accuracy of the pre-deposit amount

- Mode of payment

- Compliance with Section 107(6)

⚠️ Incorrect adjustments may result in:

- Rejection of appeal

- Issuance of deficiency memo

- Additional tax demand

📌 Key Takeaways for Professionals

🔹 Ensure correct computation of disputed tax

🔹 Maintain proper documentation of prior payments

🔹 Reconcile:

- Order amount

- Amount already paid

- Required pre-deposit

💡 Professional Tip

Before editing the pre-deposit field, prepare a detailed working sheet including:

- Total demand

- Admitted liability

- Disputed portion

- Pre-deposit calculation

- Payments already made

This helps minimize litigation risks at the appellate stage.

🚀 Conclusion

This update is a practical and taxpayer-friendly move by GSTN. It removes earlier system restrictions and aligns the portal with real-world scenarios.

👉 However, greater flexibility also means greater responsibility—accurate calculations and proper justification are now essential.