Why Quotation Management is Important for Every Business

Why Quotation Management is Important for Every Business

In today’s competitive business world, sending a professional quotation is the first step toward winning a customer’s trust and closing more deals. A quotation helps businesses clearly explain product pricing, taxes, discounts, delivery details, and terms before the final order confirmation.

Without a proper quotation system, businesses face:

- Manual calculation errors

- Delayed customer response

- Unprofessional document formats

- Poor follow-up management

- Difficult sales tracking

That’s why EASY SMART SHOP provides a complete and advanced Quotation Management System designed to simplify your sales process and improve business productivity.

EASY SMART SHOP – Advanced Quotation Management System

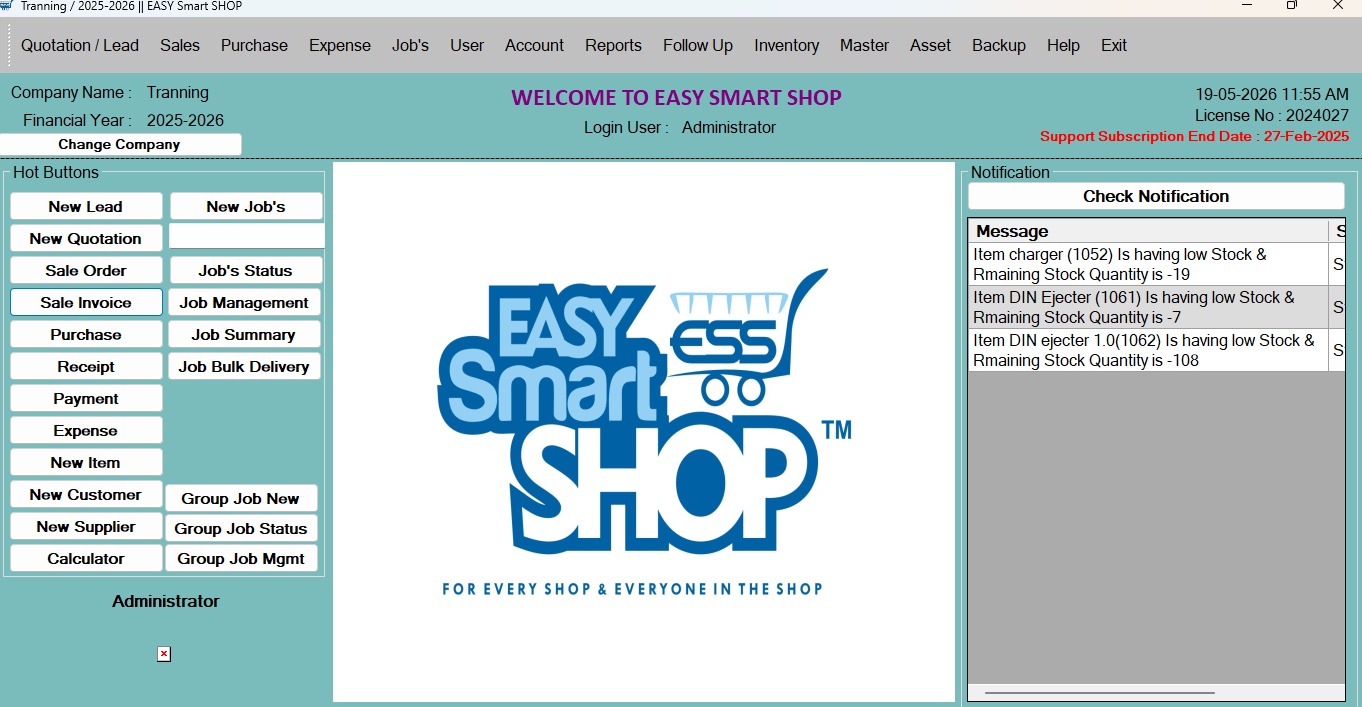

Smart Dashboard for Fast Operations

The EASY SMART SHOP dashboard gives users quick access to all important quotation and sales features from a single screen.

Dashboard Features:

- New Quotation Creation

- Sales Order Management

- Invoice Generation

- Purchase Management

- Customer Management

- Inventory Tracking

- Job Management

- Notification Alerts

- Reports & Accounts

The software is designed with a simple and user-friendly interface so businesses can work faster and more efficiently.

Complete Quotation Management Panel

The Quotation Management screen helps businesses manage all quotations in one place.

Features Available:

- Pending Quotation Tracking

- Rejected Quotation Records

- Final Quotation Management

- Customer-wise Quotation Filter

- Follow-Up Date Management

- Closing Date Tracking

- Sales ID & Invoice Linking

Businesses can easily track quotation status and follow up with customers at the right time.

Professional Quotation Creation Window

EASY SMART SHOP allows users to create detailed and professional quotations within seconds.

Powerful Features:

- Item-wise quotation entry

- GST tax calculation

- Discount management

- HSN code support

- Quantity & stock tracking

- Automatic amount calculation

- CGST / SGST / IGST support

- Subject & customer requirement notes

The software automatically calculates totals, taxes, discounts, and final invoice amounts, reducing manual errors.

Customer Detail Management

The Customer Details section helps businesses maintain professional customer records.

Information Managed:

- Customer Name

- Address

- Contact Number

- Email Address

- GST Number

- State Selection

- Reference Details

- Designation Information

This helps businesses maintain organized customer communication and accurate documentation.

Advanced Features in EASY SMART SHOP

The software includes multiple advanced features that make business operations faster and smarter.

Proforma Invoice System

Businesses can instantly convert quotations into professional Proforma Invoices.

Benefits:

- Professional invoice format

- GST-ready documents

- Faster customer approval

- Easy printing & sharing

- Sales process automation

E-Mail Proforma Invoice

The software allows direct emailing of Proforma Invoices to customers.

Advantages:

- Instant customer communication

- PDF attachment support

- Faster deal confirmation

- Paperless workflow

- Professional business impression

E-Mail Quotation Feature

Users can directly send quotations through email from the software.

Benefits:

- One-click quotation sharing

- Fast customer response

- Better follow-up process

- Improved sales conversion

Create Delivery Challan

EASY SMART SHOP also provides Delivery Challan creation for product dispatch management.

Features:

- Delivery document generation

- Dispatch tracking

- Customer delivery records

- Professional challan format

Quotation Follow-up & Updates –

Easily track quotation follow-ups and make quick updates based on customer requirements.

Quotation History Management –

Maintain a complete history of all quotations, making it easy to access previous records anytime.

Document Management –

Store and manage all quotation-related documents, PDFs, bills, and attachments in one secure place for better organization and faster access.

Terms & Conditions Management

The software allows users to add custom Terms & Conditions in quotations.

Features:

- Add custom terms

- Edit existing terms

- Save templates

- Reuse quotation formats

- Print-ready documentation

This makes every quotation more professional and legally clear.

Why Businesses Prefer EASY SMART SHOP

✔ Professional Quotation System

✔ GST Billing Support

✔ Proforma Invoice Feature

✔ Email Quotation Sending

✔ Delivery Challan Management

✔ Customer Database Management

✔ Smart Tax Calculation

✔ Inventory Integration

✔ User-Friendly Interface

✔ Faster Business Workflow

Perfect Solution For

- Retail Shops

- Wholesale Businesses

- Electronics Shops

- Mobile Shops

- Service Centers

- Hardware Stores

- Manufacturing Businesses

- Computer Shops

- Distributors

Grow Your Business with EASY SMART SHOP

EASY SMART SHOP helps businesses manage quotations, invoices, customers, and sales operations professionally from one software platform.

With advanced quotation features, automated calculations, email integration, and delivery management, businesses can save time, reduce manual work, and improve customer satisfaction.