GST Latest Update: IMS Offline Tool Comes into Effect

In a major move to enhance GST compliance efficiency, the GST Network (GSTN) rolled out the IMS (Invoice Management System) Offline Tool on 21st April 2026. This initiative is designed to simplify invoice-level activities for taxpayers and improve the reconciliation process.

Background – What is IMS?

The Invoice Management System (IMS) was introduced on the GST portal starting from the October 2024 tax period. Its key objective is to provide taxpayers with greater control over their inward supplies (purchase invoices) reflected in the system.

Under IMS, taxpayers can review and take appropriate action on invoices uploaded by suppliers through:

- GSTR-1

- GSTR-1A

- IFF (Invoice Furnishing Facility)

Available Actions in IMS include:

✔️ Accept invoice

❌ Reject invoice

⏳ Keep invoice pending

This system plays a vital role in Input Tax Credit (ITC) reconciliation by ensuring that ITC is claimed only on valid and verified invoices, thereby improving overall compliance accuracy.

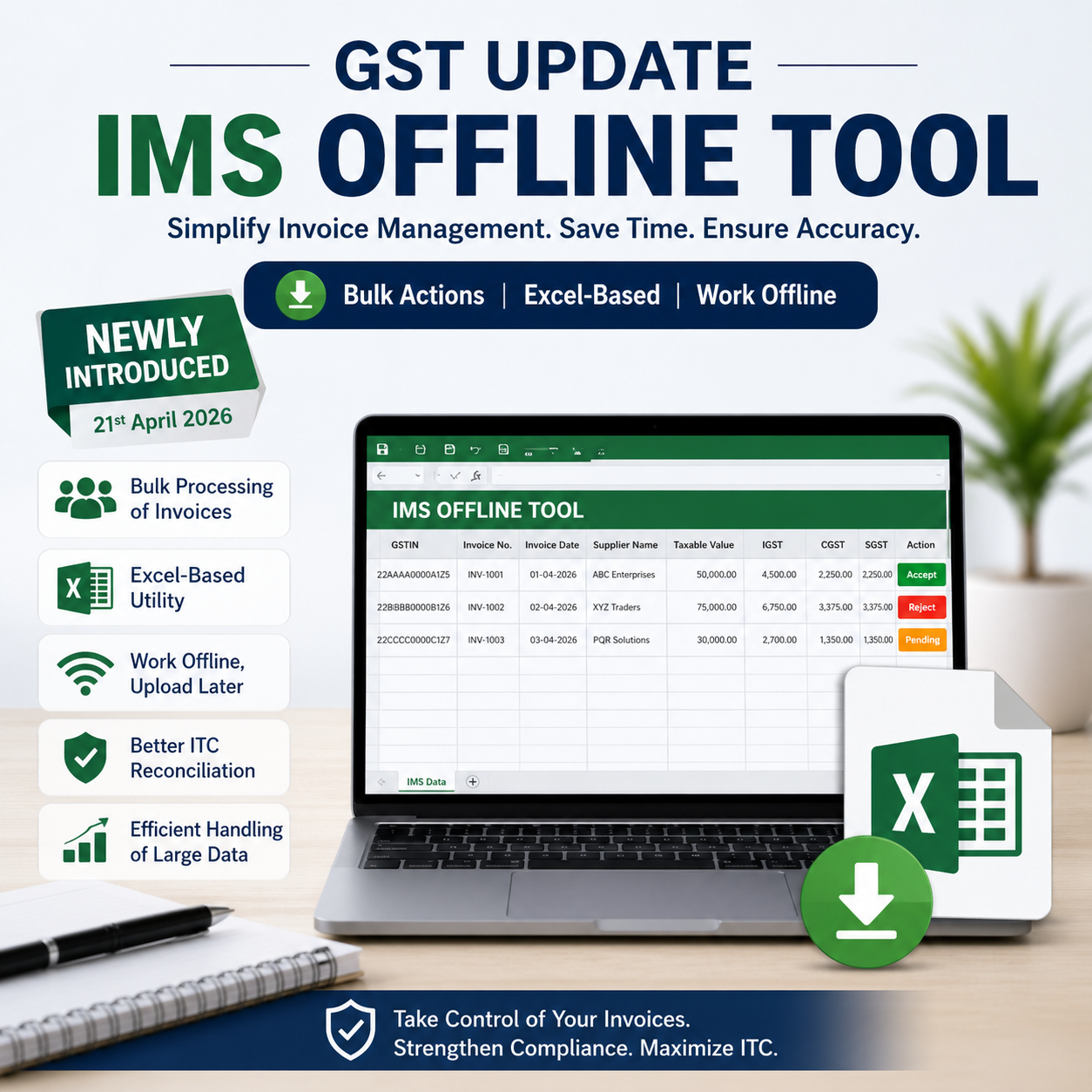

What’s New? – IMS Offline Tool

To enhance usability and address practical challenges faced by taxpayers, the GST Network (GSTN) has introduced the IMS Offline Tool.

📌 Key Highlight:

👉 Excel-based utility (MS Excel format)

👉 Designed for ease of use and bulk processing

🎯 Key Features of IMS Offline Tool

1️⃣ Bulk Processing of Invoices

Previously, taxpayers were required to take action on invoices individually through the GST portal.

Now:

👉 Download invoice data

👉 Take action in bulk (Accept / Reject / Pending)

👉 Upload the updated file back to the portal

📌 This is a significant time-saving feature, especially for:

- Large businesses

- Professionals managing multiple clients

2️⃣ Excel-Based Utility (User-Friendly)

The tool is built on MS Excel, making it:

- Easy to understand

- Familiar for accountants and tax professionals

- Usable without advanced technical knowledge

3️⃣ Offline Working Capability

👉 No need for continuous internet access

You can:

- Work offline

- Review invoices carefully

- Upload once the process is complete

📌 This helps reduce:

- Dependency on the GST portal

- Last-minute filing stress

4️⃣ Improved ITC Reconciliation

While IMS already supports ITC validation, the offline tool further enhances the process.

👉 Reconciliation becomes:

- Faster

- More accurate

- Less prone to errors

5️⃣ Efficient Handling of Large Data

For taxpayers dealing with high volumes of invoices:

👉 The tool ensures:

- Smooth data handling

- Reduced issues related to portal lag

⚠️ Important Points to Note

- The IMS Offline Tool is optional but highly recommended

- Final upload must be completed on the GST portal

- Careful review before uploading is essential

- Incorrect actions may impact ITC eligibility

Practical impact:

Practical impact: