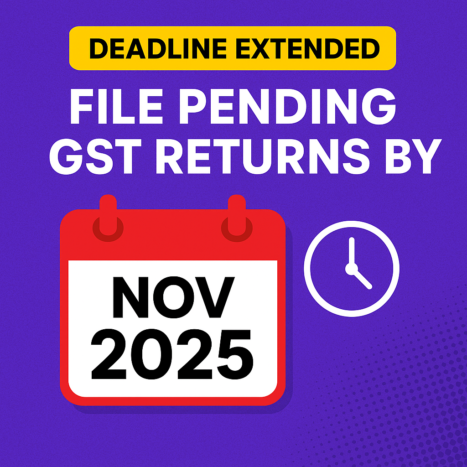

🚨 GSTN Update: Extension Granted for Filing Overdue GST Returns

🆕 Late Filing Restrictions to Take Effect from November 2025

📅 Announcement Date: 29th October 2025

📢 Issued By: Goods and Services Tax Network (GSTN)

🧾 Overview

The Goods and Services Tax Network (GSTN) has released a crucial advisory urging taxpayers to submit all outstanding GST returns before the three-year deadline from their respective due dates lapses.

This move aligns with the enforcement of Sections 37, 39, 44, and 52 of the CGST Act, amended through the Finance Act, 2023 (Act No. 8 of 2023) and made effective from 1st October 2023 via Notification No. 28/2023 – Central Tax (dated 31st July 2023).

Under this reform, returns older than three years from their statutory due date cannot be filed, marking a significant step toward clearing long-pending defaults and improving data integrity within the GST system.

⏳ What’s Changing Under the New Rule

Previously, taxpayers could file overdue GST returns for any past period — even years later — by paying the applicable late fees and interest.

Under the revised framework, however, the GST portal will automatically restrict filing of any return once three years have passed since its original due date.

To ensure a smooth transition, the effective rollout of this restriction has been deferred until the November 2025 tax period.

👉 In practical terms, this means that any GST return older than three years as of November 2025 will be permanently locked from being filed on the portal.

📢 Key Points from GSTN Advisory (29th October 2025)

Under the Finance Act, 2023, taxpayers will no longer be able to file GST returns after three years from their respective due dates. This rule applies to the following sections:

-

Section 37 – Outward Supplies (Forms GSTR-1 / IFF)

-

Section 39 – Tax Payment Returns (Forms GSTR-3B, GSTR-4, GSTR-5, etc.)

-

Section 44 – Annual Returns (Forms GSTR-9, GSTR-9C)

-

Section 52 – Tax Collected at Source (Form GSTR-8)

These provisions collectively cover major return types — GSTR-1, 3B, 4, 5, 5A, 6, 7, 8, 9, and 9C.

The three-year filing restriction will officially take effect from the November 2025 tax period, meaning any return whose original due date is before 30th November 2022 will be permanently locked from filing after 30th November 2025.

📅 Notably, a similar advisory was released in October 2024, but the implementation deadline has now been extended to December 2025 to give taxpayers additional time to regularize past defaults.

📊 Illustration of Returns That Will Be Restricted from Filing Effective 1st December 2025

| GST Form | Period Affected | Description |

|---|---|---|

| GSTR-1 / IFF | October 2022 | Outward supply details for monthly filers |

| GSTR-1 (Quarterly) | July – September 2022 | For taxpayers under QRMP scheme |

| GSTR-3B (Monthly) | October 2022 | Monthly return summarizing tax payment |

| GSTR-3B (Quarterly) | July – September 2022 | For small taxpayers under QRMP scheme |

| GSTR-4 | FY 2021-22 | Annual return for composition taxpayers |

| GSTR-5 | October 2022 | Return for non-resident taxable persons |

| GSTR-6 | October 2022 | Filed by Input Service Distributors (ISD) |

| GSTR-7 | October 2022 | Return for TDS deductors |

| GSTR-8 | October 2022 | Return for TCS collectors (E-commerce operators) |

| GSTR-9 / 9C | FY 2020-21 | Annual return and reconciliation statement |

➡️ Note: All the above returns will be permanently blocked from filing after 30th November 2025, as they exceed the three-year filing window allowed under the amended GST law.

📌 Understanding the Change

Starting 1st December 2025, any taxpayer who has not filed returns for periods older than the timelines mentioned will find the filing option automatically disabled on the GST portal.

In simpler terms:

👉 Returns due before October 2022 (for monthly filers) or before Q2 FY 2022–23 (for quarterly filers) will be permanently unavailable for submission after the cut-off date.

💡 Purpose Behind the Restriction

The introduction of this rule is intended to:

-

Eliminate long-pending non-filers and streamline inactive GST registrations.

-

Enhance the reliability and consistency of GST data and ITC reconciliation.

-

Discourage delayed or backdated filings that distort the accuracy of tax records.

-

Promote a culture of timely compliance and ensure closure of past liabilities.

⚠️ Practical Impact on Taxpayers

Taxpayers who still have unfiled GST returns for FY 2020-21, 2021-22, or 2022-23 should complete their filings without delay.

Once the restriction becomes active, these returns cannot be filed at all, even by paying penalties or late fees.

Non-compliance may lead to:

-

Input Tax Credit (ITC) mismatches for recipients

-

Issuance of demand or show-cause notices by the department

-

Possible suspension or cancellation of GST registration

🧮 Illustrative Example

Suppose your GSTR-3B for October 2022 had a due date of 20th November 2022.

Once the three-year period ends — i.e., on 20th November 2025 — the system will automatically restrict access to file this return.

After that, you won’t be able to submit it, even if you intend to comply voluntarily or pay applicable dues.

📢 Recommended Actions for Taxpayers

✅ Check & Reconcile all pending GST returns for FY 2021-22 and FY 2022-23.

✅ Submit any unfiled returns (GSTR-1, 3B, 4, 7, 8, 9/9C, etc.) well before 30th November 2025 to avoid permanent blocking.

✅ Alert clients, accountants, and teams to finalize and upload pending data without delay.

✅ Verify ITC claims, tax payments, and interest to ensure accurate compliance before filing.

No Modifications to ITC Auto-Population

No Modifications to ITC Auto-Population GSTR-2B Continues to be Auto-Generated Without Manual Input

GSTR-2B Continues to be Auto-Generated Without Manual Input New Options for Credit Note Handling Effective October 2025

New Options for Credit Note Handling Effective October 2025 Practical Example

Practical Example

Faster Refunds for low-risk and compliant taxpayers.

Faster Refunds for low-risk and compliant taxpayers. Automated Risk Score – keep returns accurate, timely and consistent to stay in low-risk category.

Automated Risk Score – keep returns accurate, timely and consistent to stay in low-risk category. No Provisional Refund if prosecution, pending SCN or appeal.

No Provisional Refund if prosecution, pending SCN or appeal. IDS Refunds also eligible for 90% provisional refund (temporary relief).

IDS Refunds also eligible for 90% provisional refund (temporary relief). Officers’ discretion limited – must record reasons if they hold back refund.

Officers’ discretion limited – must record reasons if they hold back refund. Check refund history before filing — pending cases may affect risk score.

Check refund history before filing — pending cases may affect risk score.