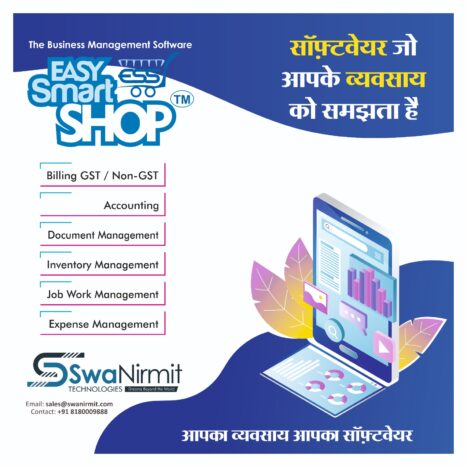

Easy Smart Shop Software – Complete Business Management Solution for Modern Businesses

In today’s fast-growing and competitive business world, managing daily operations manually is becoming difficult and time-consuming. Every business requires fast billing, accurate stock management, proper accounting, and professional reporting to run smoothly and efficiently.

To solve these challenges, SwaNirmit Technologies proudly presents Easy Smart Shop Software — a smart, reliable, and complete business management solution designed for modern businesses.

Whether you run a retail shop, supermarket, manufacturing unit, medical store, or wholesale business, Easy Smart Shop Software helps you manage your entire business digitally from one powerful platform.

Why Businesses Need Smart Management Software

Traditional business management methods often create problems such as:

- Slow billing process

- Stock mismatch and inventory errors

- Difficulty in maintaining accounts

- Manual report preparation

- Outstanding payment tracking issues

- Data loss and security risks

A professional business software solution helps businesses save time, reduce errors, improve productivity, and make better business decisions.

Easy Smart Shop Software is specially developed to make daily business operations simple, fast, and professional.

Key Features of Easy Smart Shop Software

GST & Non-GST Billing

Generate professional invoices quickly with GST and Non-GST billing support.

Fast Invoice Printing

Create and print invoices instantly to improve customer service and reduce billing time.

Inventory & Stock Management

Track available stock, low stock alerts, purchase entries, and product management easily.

Purchase & Sales Management

Manage all purchase and sales activities from one system with complete records.

Customer & Supplier Management

Maintain customer and supplier information with transaction history and balance tracking.

Accounting & Ledger Reports

Get accurate accounting reports including ledgers, profit reports, balance summaries, and more.

Outstanding & Payment Tracking

Track pending payments, customer dues, and supplier outstanding reports easily.

Barcode Support

Faster product billing and inventory handling using barcode scanning support.

Multi-User Access

Allow multiple staff members to work securely with role-based access.

Reports & Business Analytics

Generate daily, monthly, and yearly reports to analyze business performance effectively.

Job Work & Production Management

Manage manufacturing, production, and job work operations professionally.

Data Backup & Security

Keep your important business data secure with backup and recovery options.

User-Friendly Interface

Simple and easy-to-use design suitable for all business owners and staff.

Custom Print Formats

Customize invoices and print formats according to your business requirements.

Businesses That Can Use Easy Smart Shop Software

Our software is suitable for various business types, including:

- Retail Shops

- Super Markets

- Grocery / Kirana Stores

- Garments & Footwear Shops

- Mobile & Electronics Stores

- Hardware & Electrical Businesses

- Furniture Shops

- Printing Press

- Manufacturing Units

- Wholesale Businesses

- Job Work Industries

- And many more…

Continuous Updates & New Features

Technology changes rapidly, and businesses need modern solutions to stay ahead in the market.

One of the biggest strengths of Easy Smart Shop Software is continuous improvement. We regularly provide:

- New features

- Software updates

- Improved reports

- Better performance

- Latest business tools

- Modern billing solutions

This keeps your business software future-ready and efficient.

Benefits of Using Easy Smart Shop Software

✔ Faster Billing Process

✔ Better Stock Control

✔ Professional Business Management

✔ Reduced Manual Work

✔ Accurate Accounting

✔ Improved Customer Service

✔ Secure Business Data

✔ Time & Cost Saving

✔ Increased Business Productivity

Our Mission

At SwaNirmit Technologies, our mission is simple:

To make business management smarter, faster, easier, and completely professional for every business owner.

We believe every business deserves reliable software that helps them grow confidently in the digital era.

Contact Us

If you are looking for a complete business management software solution, Easy Smart Shop Software is the perfect choice for your business.

📞 Mobile: +91 8180009888

🌐 Easy Smart Shop Official Website

🌐 SwaNirmit Technologies Official Website

Start managing your business smarter with Easy Smart Shop Software today!